In the Philippines, estate settlement is governed by the Civil Code (R.A. 386), which establishes succession as the legal vehicle for the transfer of a decedent’s estate. Under Article 774, succession is defined as a “mode of acquisition by virtue of which the property, rights, and obligations to the extent of the value of the inheritance of a person are transmitted through his death to another or others either by his will or by operation of law.” While administrative paperwork may take months or years, the rights to the succession are transmitted the exact moment of the death of the decedent (Article 777).

The legal path depends on whether a valid will is left. Testamentary succession applies when the decedent leaves a will, which must comply with strict formalities as laid out under Section 1 (Wills), Chapter 2 of the Code. In its absence or with a void one, intestate succession takes place under Article 960.

Unlike other jurisdictions where one can disinherit family members on a whim, the Code protects compulsory heirs. Article 886 defines the legitime as “the part of the testator’s property which he cannot dispose of because the law has reserved it for certain heirs, who are, therefore, called compulsory heirs.” These heirs include legitimate children and descendants, legitimate parents and ascendants, surviving spouse, natural children, and other illegitimate children (Article 887).

Estate settlements can be done extrajudicially or judicially. If the decedent left no will and no debts, the heirs may settle the estate among themselves through an extrajudicial settlement. However, if the heirs cannot agree and if there is a will that must be authenticated, the estate must undergo a judicial settlement (probate), which is a court-supervised process.

The settlement is not complete until the government’s interest is satisfied. While the Civil Code governs the distribution, the National Internal Revenue Code (NIRC) dictates the tax obligations. Heirs must settle the Estate Tax before titles to land or shares of stock can be transferred to their names. Under current laws (as amended by the TRAIN Law), the estate tax is generally a flat rate of 6% of the net estate.

Partition is the final stage of estate settlement where the co-ownership among heirs is terminated and specific properties are assigned to each individual. This is governed by Articles 1078 to 1105.

Extrajudicial Settlement of Estate in the Philippines

Rule 74, Section 1 of the Rules of Court allows extrajudicial settlements of estate by agreement among the heirs. Said rule states that:

Section 1. Extrajudicial settlement by agreement between heirs. — If the decedent left no will and no debts and the heirs are all of age, or the minors are represented by their judicial or legal representatives duly authorized for the purpose, the parties may without securing letters of administration, divide the estate among themselves as they see fit by means of a public instrument filed in the office of the register of deeds, and should they disagree, they may do so in an ordinary action of partition. If there is only one heir, he may adjudicate to himself the entire estate by means of an affidavit filled in the office of the register of deeds. The parties to an extrajudicial settlement, whether by public instrument or by stipulation in a pending action for partition, or the sole heir who adjudicates the entire estate to himself by means of an affidavit shall file, simultaneously with and as a condition precedent to the filing of the public instrument, or stipulation in the action for partition, or of the affidavit in the office of the register of deeds, a bond with the said register of deeds, in an amount equivalent to the value of the personal property involved as certified to under oath by the parties concerned and conditioned upon the payment of any just claim that may be filed under section 4 of this rule. It shall be presumed that the decedent left no debts if no creditor files a petition for letters of administration within two (2) years after the death of the decedent.

Based on the rule, extrajudicial settlement of an estate is legally permissible only when the decedent has died intestate (without a will) without leaving any outstanding debts, and all heirs are of legal age—or are minors duly represented by authorized guardians—who unanimously agree to the division of the estate through a public instrument filed with the Registry of Deeds.

What is a Deed of Extrajudicial Settlement of Estate?

A Deed of Extrajudicial Settlement of Estate is a public instrument (i.e., as mentioned under Rule 74, Section 1) executed by the heirs of a decedent who privately agree to divide the estate among themselves without undergoing a lengthy court trial.

For a sole heir, an Affidavit of Self-Adjudication is the legal counterpart to a deed and serves as a formal sworn statement wherein the affiant declares the status as the only heir of the decedent and, by virtue of that fact, adjudicates the entire estate to himself.

Key Components of a Deed of Extrajudicial Settlement of Estate

As a legal instrument, a Deed of Extrajudicial Settlement of Estate must contain specific elements in order to be valid, enforceable, and registrable. While no standard form is prescribed, the following are indispensable:

1. Deed Title

This serves as the formal designation of the instrument, identifying its legal nature as a “Deed of Extrajudicial Settlement of Estate” or, in the case of a sole heir, an “Affidavit of Self-Adjudication.” It must also reflect the scope of the transaction, such as including “with Absolute Sale” or “with Waiver of Rights,” if the settlement involves a secondary transfer of interest.

2. Parties Clause

This identifies the heirs of the decedent and establishes their legal capacity and relationship to the deceased. It must state the full names, civil status, and residences of all participants, ensuring they are all of legal age or duly represented by legal or judicial guardians.

3. Antecedent Facts

These provide a jurisdictional basis for the instrument by reciting the fact of death and the decedent’s last known residence, among other details. It must include a categorical declaration of intestacy, affirming the absence of a last will and testament, and a formal statement that the decedent left no outstanding debts.

4. Inventory and Valuation of Estate Properties

This provides a technical and exhaustive list of the assets. Real properties must be described with precision, citing Transfer Certificate of Title (TCT) numbers and Tax Declaration details. Personal properties must include specific identifiers such as bank account numbers or stock certificate details.

5. Modes of Partition

This constitutes the dispositive portion of the deed, where the heirs specify the manner in which the estate is to be divided. It terminates the co-ownership by assigning specific portions, lots, or shares to each heir. It must reflect a unanimous agreement, as any disagreement in the mode of distribution would necessitate a shift to a judicial action for partition.

6. Other Additional or Secondary Transactions

The deed may also incorporate secondary acts like Absolute Sale, Donation, or the Waiver of Rights to simultaneously transfer inherited interests to co-heirs or third parties. This ensures a clear chain of title for the Registry of Deeds and the correct assessment of both Estate and secondary transfer taxes.

7. Publication and Tax Compliance Undertakings

These state the heirs’ formal undertaking to comply with the publication requirement and the commitment to settle all applicable estate taxes under the National Internal Revenue Code (NIRC), which serve as conditions precedent to the valid registration of the deed.

8. Representations and Warranties

Under this clause, the heirs collectively guarantee the veracity of the facts stated in the deed and the legitimacy of their claims to the estate. This also provides a mutual warranty against eviction and hidden encumbrances and binds co-heirs to settle any claims that may arise after the partition.

9. Signatures and Thumbmarks

All heirs must sign the instrument; in cases where an heir is illiterate or physically unable to sign, a thumbmark must be affixed and properly witnessed. These marks of authentication are vital for the Notary Public to certify that the parties appeared personally and that the deed is their free and voluntary act and deed.

10. Documentary Stamp and Revenue Notations

These include notations required for the deed’s legal admissibility and effectivity, particularly the payment of the Documentary Stamp Tax (DST). Notations of the BIR Certificate Authorizing Registration (eCAR) are often referenced or in the margins to prove that the government’s share has been satisfied.

11. Annexes

These consist of the vital supporting documents that are incorporated by reference into the deed to prove the recitals made by the heirs. These typically include the Death Certificate, Birth Certificates or Marriage Contracts proving filiation, and Certified True Copies of the titles or tax declarations.

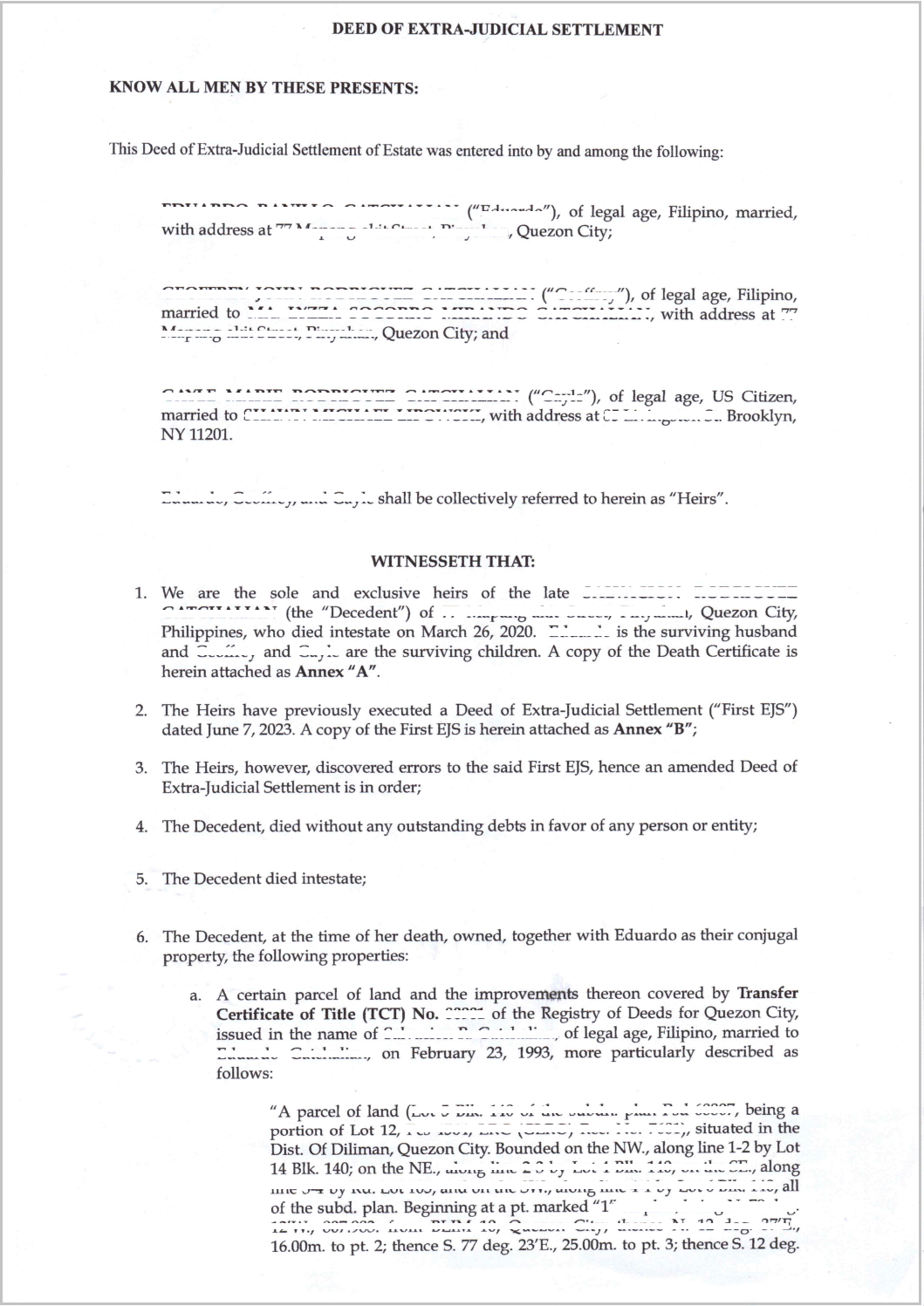

Deed of Extrajudicial Settlement Sample