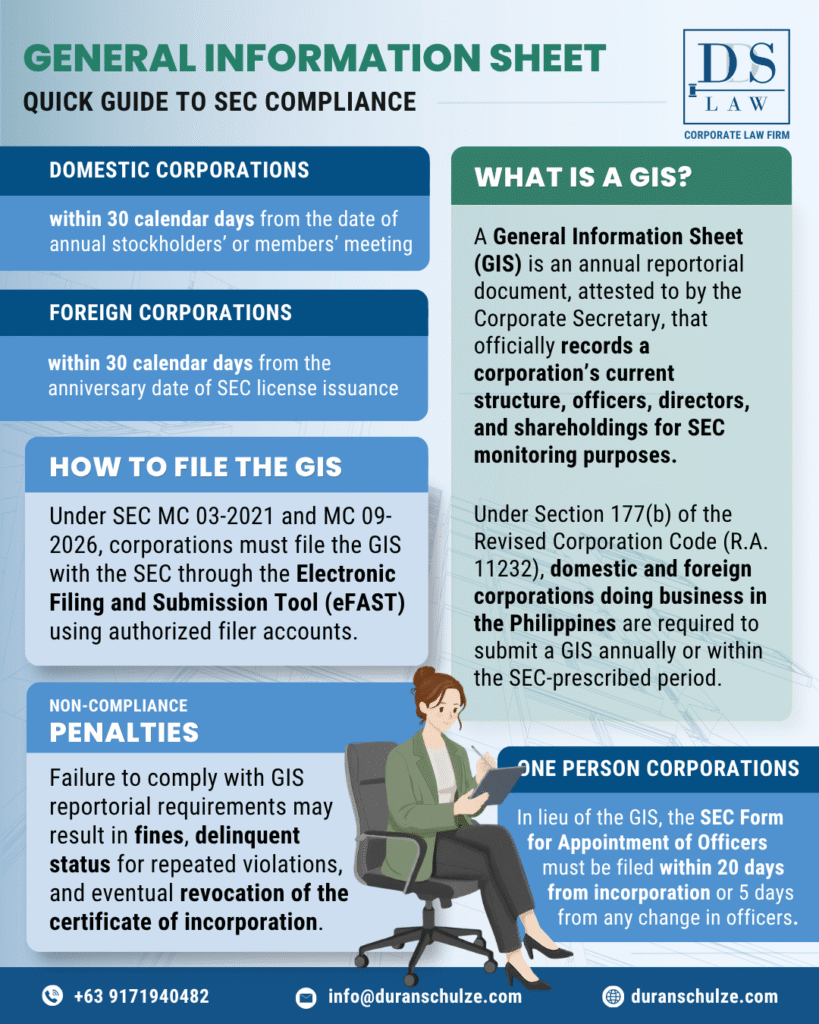

Penalties for Non-Compliance with GIS Filing Requirements

Non-compliance with GIS reportorial requirements triggers pecuniary fines (currently based on SEC Memorandum Circular No. 6-2024) and may result in delinquency status and revocation of license.

Late Filing Penalties

For domestic stock corporations, including One Person Corporations (OPCs), fines for late filing of the General Information Sheet (GIS) range from PHP 5,000 to PHP 45,000, depending on retained earnings, fund balance, or equity, and the number of offenses. For domestic non-stock corporations, fines range from PHP 5,000 to PHP 27,000.

For foreign stock corporations (e.g., branches, representative offices, and ROHQs), fines for late filing of the GIS range from PHP 10,000 to PHP 54,000, depending on accumulated income (AI), fund balance, members’ equity, and the number of offenses. For foreign non-stock corporations, fines range from PHP 5,000 to PHP 45,000.

Non-Filing Penalties

For domestic stock corporations, including One Person Corporations (OPCs), fines for non-filing of reportorial requirements (i.e., more than one year after the prescribed deadline) range from PHP 10,000 to PHP 54,000, depending on retained earnings, fund balance, or equity, and the number of offenses. For domestic non-stock corporations, fines range from PHP 10,000 to PHP 36,000.

For foreign stock corporations (e.g., branches, representative offices, and ROHQs), fines for non-filing of reportorial requirements (i.e., more than 60 days after the anniversary of the SEC license issuance) range from PHP 10,000 to PHP 90,000, depending on accumulated income (AI), fund balance, members’ equity, and the number of offenses. For foreign non-stock corporations, fines range from PHP 10,000 to PHP 54,000.

Delinquency Status

Under Section 177 of the RCC, the SEC is empowered to place corporations under delinquent status in case they fail to file their reportorial requirements (including the GIS) three (3) times either consecutively or intermittently, within five (5) years.

Revocation of License

From the receipt of the Order of Delinquency issued by the SEC, corporations have six (6) months to file a petition to lift the order, otherwise resulting in the revocation of the Certificate of Incorporation and effectively dissolving the corporation’s legal existence (SEC Memorandum Circular No. 19-2023).

Best Practices for Maintaining GIS Compliance

In the current corporate regulatory climate in the Philippines, the Securities and Exchange Commission (SEC) has transitioned toward a highly digitized, almost zero-contact enforcement model that demands proactive oversight throughout the fiscal year. Here are some of the best practices that corporations can always adopt:

1. Adopting Strategic Corporate Governance

Strategic governance requires moving beyond reactive reportorial filing. By institutionalizing regular internal reviews, corporations can avoid the common technical errors that lead to reversions of submissions in the eFAST system.

2. Maintaining an SEC Compliance Calendar

A standard compliance cycle for a corporation with a fiscal year ending December 31 typically follows a rigorous trajectory. It is important to note that while the GIS is an annual filing, beneficial ownership updates are now event-driven requirements that must be handled in real-time.

3. Empowering the Corporate Secretary or Compliance Officer

While the Corporate Secretary acts as the primary custodian of corporate records and the mandatory signatory of the GIS, a Compliance Officer may also be appointed to bridge the gap between board-level resolutions and regulatory submissions.

GIS Compliance Frequently Asked Questions (FAQs)

For additional reference and guidance, here are some of the most frequently asked questions about compliance with the General Information Sheet (GIS) requirements:

1. Who signs the General Information Sheet (GIS)?

The GIS must be signed and attested to by the Corporate Secretary, who assumes legal responsibility for the veracity of the information. However, for One Person Corporations (OPCs), the single stockholder or the appointed President signs the counterpart Appointment Form.

2. Does the GIS require notarization?

Yes, the GIS must be verified under oath, meaning the Secretary’s Certificate page must be duly notarized by a commissioned Notary Public before the scanned PDF version is uploaded to the eFAST system.

3. What happens if the annual meeting is not held?

If the annual meeting is not held on the date fixed in the Bylaws, the corporation must still file a “pro-forma” GIS no later than January 30 of the following year, indicating that no meeting was held. Once the meeting is eventually held, you then file a “New” or “Amended” GIS within 30 days of that actual meeting.

4. Is GIS filing required after a special meeting?

A new GIS is not necessarily required after every special meeting; however, if a special meeting results in material changes to the corporation—such as the election of a new director to fill a vacancy or a change in officers—an Amended GIS must be filed within seven (7) to thirty (30) days (depending on the specific nature of the change) to reflect the updated information.

5. Can the GIS be amended after filing?

Yes, an Amended GIS may be filed via the eFAST portal within thirty (30) days from the occurrence of any material change, such as the election of new directors, the resignation of an officer, or a change in the corporation’s principal business address.

6. Are partnerships required to file a GIS?

Partnerships are not obligated to file a GIS but are required to file an Amended Articles of Incorporation in case of changes in the structure and operations, such as a transfer to a new location.